Полная версия

Полная версияПолная версия:

Kyle Inan Evolution of the International Monetary System

- + Увеличить шрифт

- - Уменьшить шрифт

Kyle Inan

Evolution of the International Monetary System

“A historical analysis of the Classical Gold Standard System, the Inter-War Period, the

Bretton Woods Agreement & the International Monetary Order of the Post-1973 Era”

It is within the purview of this book to analyze the emerging monetary policy trends following the establishment of the Bretton Woods System that brought about the creation of the International Monetary Fund (the IMF) and the International Bank for Reconstruction and Development (IBRD) to assist member countries with restoring their balance-of-payments equilibrium through the enactment of fixed exchange rates currency regime and through credit lending to poor countries in need. The main purpose for introducing these systems was to concretely establish a “par-value” exchange rate among member countries in which they would peg their respective currencies to the U.S. dollar.

Furthermore, the book aims to explain the several important reasons for the failure of the world monetary reform after the collapse of the Bretton Woods System in an era compounded by the problems of shortage of U.S. dollars in the world economy as well as the recurring trade deficits that forced European countries to reconsider their commitment to the fixed exchange rate system. The book explores the reasons that led to the creation of “the European Monetary System (EMS)” as well as the European motives behind creating a single unit of currency, vis-à-vis the “Euro.” It concludes with an overall analysis of the historical evolution of the international monetary system.

The Historical Evolution of the International Monetary System

Since the inception of the social dynamics crisis caused by the Napoleonic Wars until the wake of the Industrial Revolution in the eighteenth century, there was little room for global interaction among states as there was no stimulus to engage in international trade. The absence of a regulatory system around the globe followed by the exploitation of resources in underdeveloped countries by hegemonic powers, laid the foundations for excess capital mobility giving rise to disruptive shocks to the international system.

The lack of a worldwide commercial network and uncontrolled economic activity pushed countries away from the balance-of-payments equilibrium. The prospects for international trade remained relatively low; especially without the existence of institutions capable of supporting markets both at the domestic and international levels.

By the end of the nineteenth century, the unilaterally adjusted monetary statutes of many nations around the world had created a set of conditions for the minting and circulation of two distinct metallic mediums of exchange: gold and silver. Countries that allowed the simultaneous circulation of gold and silver both as acceptable units of currencies in their economies were operating under a system that was known as “bimetallic standards.” At the time, with the exception of Britain and France, almost all of the European countries were operating on silver standards. In essence, Britain had differed from other countries that have previously adopted the silver standard mainly because the British economy had been using gold as the standard currency from the start of the century.

Similarly, France was also an exceptional case in this era since the French monetary laws were representative of bimetallic statutes. However, the privilege of allowing the simultaneous circulation of both gold and silver presented its own challenges.

A significant historical example of this dilemma was during the last years of the nineteenth century when 14.5 ounces of silver were being traded roughly for an ounce of gold in the market place in France.

From time to time, whenever the price of gold in the world market rose more than that of silver’s, let us say up to a point where 15 ounces of silver were being traded in exchange for an ounce of gold, then such a market price of gold would create an incentive for arbitrage. Thus, the arbitrager would have a window of opportunity to be able to import at the previous quantity of “14.5” ounces of silver and have it coined at the mint price. Then initially, that silver coin would be traded in exchange for an ounce of gold and the gold (i.e. the extra half ounce of silver) that the arbitrager had earned in the domestic market would be exported at a cheaper rate and a be sold for 15 ounces of silver on foreign markets.

Ultimately, the arbitrager would continue to export gold and double his earnings insofar as the market ratio had stayed considerably above the mint ratio.

Conversely, if the market ratio were to fell below the mint ratio (i.e. after a few discoveries of new gold reserves) then arbitragers would import gold and export silver. This window of opportunity was called the “Gresham’s Law”, where the bad money with a lower commodity value, vis-à-vis silver, would drive out the one with the higher commodity value, vis-à-vis gold.

In the last quarter of the nineteenth century, the shortcomings of the prevailing bimetallic system had divided the Western countries among themselves. This took place especially between those who were operating solely on silver as the only medium of exchange and those who were solely operating on gold as well as those operating on bimetallic standards; on both gold and silver. This situation was causing many of the industrializing European economies to experience growing difficulties in international transactions as well problems in creating a smoothly functioning domestic economy.

As Britain and the United States, two countries that were fully committed to gold, emerged as the world’s most prominent financial and industrial powers with the advent of the industrial revolution by the end of the century, some of the few countries with silver standards have decided to peg their silver coins to the gold standards of those countries. “By the beginning of the twentieth century, there had finally emerged a truly international system based on gold.” (Eichengreen, 2008, pg. 19)

This system was called the “Classical Gold Standard System.”

The Classical Gold Standard System (1880-1914)

“The breakdown of the international gold standard was the link between the disintegration of world economy since the turn of the century and the transformation of a whole civilization in the thirties.” (Polanyi, The Great Transformation, pg. 20)

Historically, the most famous and durable international monetary system was the Gold Standard System largely because several things have served as a medium of exchange in the early days of the nineteenth century. For instance, some of those things were cattle, sheep, wine, jewelry, and diamonds as well as many other precious stones that were being bought and sold in the markets. However, metal coins had some unique characteristics to be more acceptable; (I) First of all, metal coins were easy to divide (divisibility), (II) Secondly, coins were also very durable (durability), (III) Thirdly, the supply of precious metals such as gold and silver were stable to a great extent, and their final and their most important feature which served in the facilitation of daily transactions (IV) was their recognizability. It is primarily for these reasons that metal coins became the most popular medium of exchange over time driving out others.

In addition to the gold’s ability to serve, as an important medium of exchange, there were also three main rules to the Gold Standard; (i) All countries had to fix the price of gold in terms of their domestic currency. This was called the “mint price of gold.” (ii) Governments had to support the mint price for transactions with the public to assure that the mint price equaled to the market price of gold. Because, in the event the market price is higher (Market Price > Mint Price) than the mint price; then people would buy the gold from the government (i.e. from the Treasury Department of a given country) and the supply of gold in the market would go up while the market price of gold would go down. The opposite of this would happen whenever the market price of gold was lower than the mint price (Market Price < Mint Price). In that case, people would choose to sell the gold to the government and the supply of gold in the market would go down whereas the market price of gold would eventually go up.

A third most striking feature of the Gold Standard System was (iii) the fact that the melting of gold coins was legal. This would assure that the value of gold coins was same for monetary and non-monetary purposes.

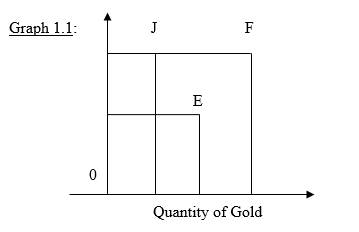

At this point, some of us might inquire about the conditions as well as the factors that determine the value of money supply under the Gold Standard. An illustrative graphical example would help us explain the key determinants of the money supply of gold under this system.

Graph 1.1 shows that, the quantity of gold demanded for non-monetary purposes will go down and the quantity supplied of gold is also expected to increase after an increase in the price of gold. Under the Gold Standard System, the government will fix the mint price above the Po level to assure that there is an adequate supply of gold to make coins out of. At a mint price of Pm, the quantity demanded of gold for monetary purposes is the distance between the origin and point Q1, whereas the quantity supplied of gold equals the distance between the origin and point Q2. In this case, the distance between Q1 and Q2 or the range between points E and F will be the gold used in the making of coins. (i.e. excess supply of gold available for gold coins.)

Under the Gold Standard System, the value of money supply can also shrink or expand based on the demand for gold for non-monetary purposes and the supply of gold. Specifically meaning that shifts in demand for gold for non-monetary purposes or the supply of gold curve can create a change in the money supply.

There are three main reasons that would cause a significant shift in the demand curve. These are as follows: (1) if there is an increase in the income of consumers, (2) if there is a change in the expectations of future prices, and if (3) there is a change in the prices of related goods and services. Since an increase in demand for gold for non-monetary purposes can cause the money supply to decline, if the supply of gold increases after a gold rush (i.e. The U.S. California Gold Rush of 1848-1855) then a shift in the supply of gold curve can also be observed.

To summarize, there are primarily three distinct factors that can cause a shift in the supply of gold curve. The three factors are: (a) If there is an increase in the number of producers; for instance, if new gold mines are discovered. (b) If the cost of production changes; for instance, if transportation becomes cheaper. (c) If there is a considerable change in the technology of production; for instance, it might become easier and less costly to extract gold with newly advanced technology.

Furthermore, a most remarkable feature of the gold standard system was its included benefits at the operational level. For instance, the money supply was independent of any government action mainly because the money supply would grow or expand at the same rate (simultaneously) with the gold supply. If there were no new discoveries of gold, then there would not be an expectation for an increase in the money supply.

Since governments had no control over the money supply under the Gold Standard, due to the aforementioned reasons, they would not be able to arbitrarily print more money and cause inflation. Therefore, there was virtually no possibility of inflation under this system. In other words, this system had promised long-term price stability to its owner, which could be described as its most significant benefit.

A second benefit of the Gold Standard was its unparalleled ability to cure its own disease, even in times of inflation. For instance, under inflationary situations, we would normally experience an increase in the price of goods and services and a decrease in gold prices. As a reaction to the change in the price of gold, producers in the economy would switch their resources to the production of goods and services instead of gold and the supply of gold would go down. As less gold is supplied, the prices would go down. Therefore, under the Gold Standard System, there was also a double attack on inflation.

A third most noticeable benefit of the Gold Standard was the “Law of One Price.” This meant that there would be a tendency for all countries under the gold standard to have the same general price levels. As an example, if we were to assume that there were two countries (A & B) with general price levels being PA and PB respectively, and if PA > PB then, under free trade conditions, country A would import goods and services from country B and pay for those imports in terms of gold. In the outcome, for country A, goods and services would arrive and gold would be lost from that country. After a while, PA would start declining. Concurrently, in country B, goods and services would be lost after gold is gained following the transaction. After a while, PB would increase. Eventually, the prices would be equal to each other. (PA = PB)

At this point, we might be inclined to ask ourselves such questions as “What went wrong with the Gold Standard System” or “Why was it dismissed in the first place if it promised such numerous advantageous compared to other international monetary systems?”

In essence, a deeper examination into the intricacies of what is called the “price-specie-flow” mechanism will provide insights into this question and help us clearly understand the actual causes in explaining the deficiencies of the Gold Standard System leading up to its collapse after its abandonment by the United States and Britain in 1931.

Price-Specie-Flow Mechanism under the Gold Standard

During the last half of the nineteenth century, the persistent outflow of capital, along with the simultaneous rise in interest rates around the world has necessitated the establishment of a price-specie-flow mechanism. This system, founded by David Hume, intended to coordinate capital flows and help central banks restore their balance-of-payments equilibrium.

By proposing this mechanism, Hume argued against the idea of having countries strive constantly to maintain a positive balance of trade. The following logic behind this approach was whenever a country had a balance of trade surplus; it would attract a certain quantity of gold in the same amount that the value of exports exceeded the value of imports. Similarly, the opposite of this situation would happen in countries running a trade deficit. This would mean that there would be a gold outflow in the same amount that the value of imports exceeded the value of exports.

In the absence of a monetary authority to regulate the quantity of gold in circulation, the money supply in the country running a positive balance of trade would increase while the money supply would decrease in the country running a trade deficit. Then, based on the principles of quantity theory of money, the country with the money surplus would experience inflation as well as a simultaneous increase in the prices of goods and services, whereas the country with the money shortage would go through a period of deflation after devaluation of goods and services. In essence, the emergence and the implementation of the price-specie-flow mechanism came with the idea of allowing gold to be the only currency in the world (or any other paper currency convertible into gold that would circulate in lieu of other metals.

The most dynamic and remarkable characteristic of this system was its “durability” which was concretely based on the premise of completely abolishing the imposition of import controls and thereby purporting to effectively facilitate the cross-border of goods and services around the world.

For instance, in countries where this system was adopted, each time a commodity was exported, the exporter of that good would receive payment in gold and the importer purchasing certain merchandise abroad, would make payment by exporting gold. For a country with a trade deficit, the number of imports would exceed the number of exports. The deficit country would then experience a significant gold outflow. “With less money (gold coin) circulating internally, prices would fall in the deficit country. With more money circulating abroad, prices rose in the surplus country. The specie flow thereby produced a change in relative prices (hence the name “price-specie-flow model”). (Eichengreen, 2008, pg. 24)

In return, domestic residents would decrease their purchase of goods and services since imports would become more expensive whereas the foreign residents would increase their purchase of goods and services since imported goods would become less expensive for them. While the country running a balance of payments deficit would experience a rise in its exports and a decline in its imports until up to a point where the balance of trade is restored. This formulation of the balance of payments equilibrium created by Hume proves us the multiple benefits as well as the way in which the gold standard system has operated.

In addition to its ability to restore the balance of payments equilibrium in countries with a trade deficit, the high level of openness granted by the gold standard system had also served to expedite the process of economic integration which mostly benefited the world's leading exporters. Even though this system supremely favored Britain as the vanguard of this system. “Because, London was the center for the world’s principal gold, commodities, and capital markets, because of the extensive outstanding sterling-denominated assets, and because many countries used sterling as an international reserve currency (as a substitute for gold), it is argued that the Bank of England, by manipulating its bank rate, could attract whatever gold it needed and, furthermore, that other central banks would adjust their discount rates accordingly.” (Braga de Macedo & Eichengreen & Reis, 1996, pg. 17)

Therefore, it could just as easily be argued that the Bank of England had the financial prowess and the capacity to exert a powerful pressure on the price levels as much as on the money supplies of other countries that were adhering to the rules of the gold-standard.

Contrary to its financial comparative advantages, the gold standard system also had three distinct shortcomings. Costs of this system included the tricky position that governments had to deal with, which forced countries to obey a set of stringent rules and surrender the control of their money supply. For instance, under this system, (I) countries were expected to fix the mint price at a par value and legalize melting of gold coins which were basically unfavorable requests for countries that were short of gold reserves at the time. Another pitfall of this system was the fact that (II) one metal was given too much importance which essentially favored countries with gold mines than those without, which also turned it into a biased system.

Nevertheless, the greatest deficiency of this system was (III) whenever a member country would decide to break the rule, it was set to gain from it. For instance, if we were to suppose that the general price levels are greater in country A than in country B (if PA > PB) and if country A was to quietly break the gold standard rule and increase its money supply (even if it does not have enough gold), then it would still keep on importing goods and services from country B and continue to pay in gold while maintaining higher price levels. Thus, according to the rules, if a country was running a trade deficit, it had to allow a certain amount of gold outflow until its price level was restored to the par value exchange rate of other countries. Some countries in Europe, such as France and Belgium that were operating on the gold standard system, chose not to follow this rule.

An example of a case where this rule was strictly observed was the case of the Central Bank of England, also known as the Bank of England. During the gold standard era, the Bank of England engaged in a leadership position as the most influential mechanism that would enforce the gold-standard regime. It has done so by strategically utilizing its monetary policies to maintain a certain level of gold convertibility.

In response to the demands of the Bank of England, other central banks in Europe acceded to the new policies it imposed by and assumed a passive stance. This was largely because of the benefits that they were able to accrue by clinging onto the sterling as the reserve asset. “Britain financed exports and imports in sterling bills, other countries their third-country trade also in sterling bills. Other countries thus had to hold balances in sterling.” (Kindleberger, 1993, pg. 71)

In addition, the Bank of England’s persistent agenda to uphold its dominant status as the central monetary authority during the era of the classical gold standard was further advanced by its extensive monetary operations that encouraged global trends such as; increasing short-term capital mobility and motivating central banks to push domestic rates downwards with the inflow of gold into these banks. Despite the Bank of England’s relatively scarce gold reserve, central banks had to continue to yield to the pressures exerted by it as they had a limited ability to effectively change their own monetary conditions, much less the international order itself. “On this showing, the Bank of England set the level of world interest rates, which accounts for the fact that national interest rates moved up and down together, while other countries had power only over a narrow differential between the domestic level and the world rate.” (Kindleberger, 1993, pg. 73)

In response to the policies enforced by the Bank of England, insolvent central banks that suffered a significant loss in their gold reserves resorted to their domestic asset holdings so that they could push interest rates upwards, which would then attract short-term capital and limit the outflow of fresh capital. In turn, this reactionary policy would strengthen their domestic economies.

In addition, under the gold standard regime, sterling bills were the only worldwide-accepted currencies that also simultaneously retained the privilege of substituting for real money in other European countries.

While the Bank of England, as the central decision-making monetary authority of the classical gold standard era, had unlimited access to international markets. This allowed it to arbitrarily determine national interest rates of other countries as well. Therefore, it would not be a far-fetched argument to claim that the classical gold standard was after all a system based completely on the British sterling.

With the outbreak of WWI, governments and central banks around the world were forcefully confronted with a need to finance high levels of military expenditures with an extremely limited source of tax revenue. Driven by the need to out compete each other in the race for war, many belligerent countries have gradually started abandoning the gold standard to issue un-backed paper currencies (which then would cause massive hyperinflation levels in these countries) while the Bank of England had temporarily suspended gold convertibility which meant that it had abolished the gold standard until after the war.

The Inter-war Period (1918-1939)

At the onset of WWI, most industrialized nations of Europe have started issuing fiat currencies (un-backed paper) in an effort to fuel the war machine. This was a period in which precious metals such as “gold” and “silver” had become a critical resource for the procurement of war material. As a consequence of the rising value of gold and silver, governments have pursued protectionist policies to prohibit the export of such precious metals while continuing to issue fiat currencies without any value.

The arbitrary creation of these currencies to support war efforts at different rates has caused wide variations in the exchange rates among European countries to the extent that some had faced severe hyperinflation in their national economies. Some of the countries like; Germany, Hungary, Austria, and Poland of which hyperinflation had taken a very heavy toll on, have made several attempts to re-establish gold convertibility to fix the fundamental disequilibria in their balance of payments. However, the British Sterling, which had been providing the strongest foundation for the harmonization of economic policies prior to the outbreak of WWI, was no longer enjoying its hey day.